This Trust Could Offer Some Florida Couples a Windfall in Tax Savings

Highly appreciated assets are a blessing and a curse. If you have a big stock position, a second home or other property you’ve owned for years, a longstanding family business, or any other long-held asset, you are that much richer when you sell. But you could also owe a lot in taxes on that realized wealth.

A relatively new planning tool—the Florida community property trust (CPT)—may help some married couples dramatically reduce those taxes. But these trusts aren’t for everyone.

(This summary is largely based on two articles published in the Florida Bar Journal, which are recommended reading for anyone interested in a more nuts-and-bolts discussion.)

Separate vs. Community Property States

In most states (including MA, NY, and CT) ownership of an asset is determined by how that asset is titled. Assets acquired during marriage aren’t automatically treated as jointly owned property.

In the nine community property states, assets acquired during marriage are considered community property. Each spouse owns an equal one-half share of community property.

Five states determine asset ownership by title, but allow married couples to place assets into a specially drafted trust and elect community property treatment for those assets. Florida became one of these “opt-in” states in 2021.

A step-up for both spouses

The upside to a CPT? It allows both spouses' shares of appreciated assets to receive a full step-up in tax basis when the first spouse dies.

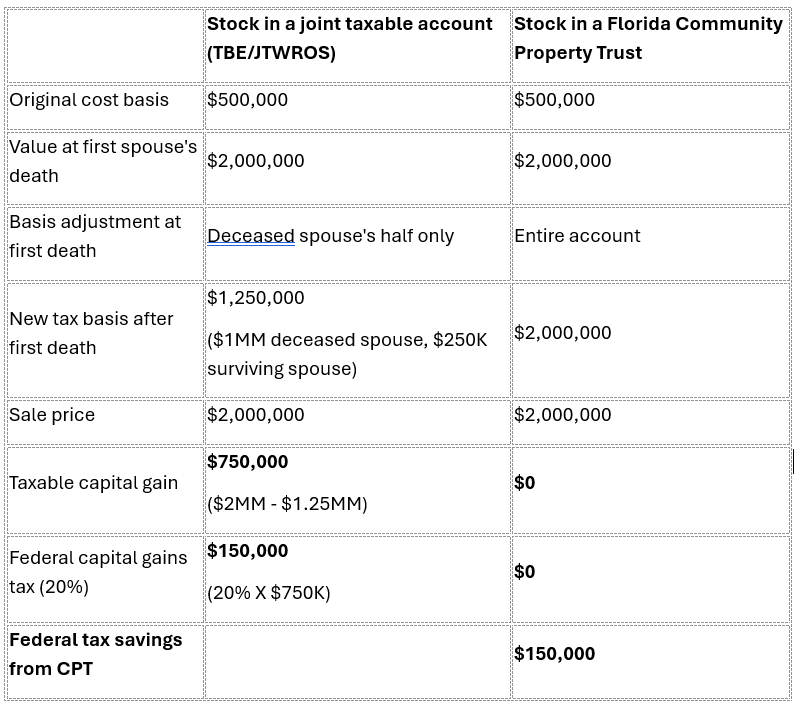

To see just how much can be saved in taxes (comparison below), consider a married couple with Florida residency who own a stock position that originally cost $500,000 and is now worth $2 million. Assume one spouse dies and the surviving spouse sells the entire stock position.

In a taxable account outside of a CPT, the surviving spouse will owe $150,000 in federal capital gains taxes. No tax is owed on the inherited share, which gets a cost basis step-up. Tax is owed on the $750,000 portion the surviving spouse owns and isn’t stepped up.

The picture is much different with the stock inside a CPT. Both the inherited half and the half owned by the surviving spouse get a step-up in cost basis. Capital gains tax is owed only on the gains earned between the death of the spouse and the sale of the stock, which could be minimal to none.

For this couple, that’s a tax savings of about $150,000. Depending on the assets inside the trust, the savings can easily extend well into six figures.

Capital Gains Tax Outside and Inside a Community Property Trust

This example assumes the account is jointly owned, qualifies for a full basis adjustment under a properly structured Florida community property trust, the stock is sold immediately after the first spouse's death with no additional appreciation, and a 20% federal capital gains tax rate, and ignores the 3.8% net investment income tax and any transaction costs.

The title tells the story

If an asset is owned solely by one spouse, then 100% of that asset generally receives a basis adjustment on that spouse's death. A CPT is most valuable when it provides a basis adjustment on both spouses' interests in assets that would otherwise receive only a partial adjustment.

When a CPT makes sense

The best candidates for a CPT are often:

Married couples with substantial unrealized capital gains in taxable assets

Couples who expect to hold those appreciated assets until one spouse dies

Families who want the flexibility to sell appreciated assets after the first spouse's death

Owners of long-held brokerage accounts, investment real estate, family businesses, or concentrated stock positions

Because today's federal estate tax exemption is so high—about $15 million per person as of 2026—many affluent families won't owe federal estate tax. But those same families may own decades' worth of appreciated investments that could generate substantial capital gains taxes if sold. This capital gains issue is exactly what a CPT is designed to address.

Image created by ChatGPT

When a CPT May Not Make Sense

Although a CPT can produce substantial tax savings for the right couple, it can also create unnecessary complexity when misapplied.

A CPT is generally offers little to no advantage to:

Couples with little unrealized appreciation in taxable assets

Those with assets that have declined in value

Situations where the primary objective is asset protection rather than tax planning

Couples whose broader estate plan or homestead planning would become unnecessarily complicated by a CPT (see below)

Notice that a community property trust works both ways. It can create a double step-up in basis, but it can also create a "double step-down." If an asset has fallen below its cost basis, placing it in a CPT may actually eliminate a future tax loss that otherwise could have been used to apply against gains elsewhere.

The tradeoffs

Florida CPTs come with many complications that are spelled out in much more detail here. But a few broad principles apply.

You're Changing Ownership Rights

Community ownership gives each spouse an equal one-half interest in community property. This can affect how assets are treated at death or in divorce. Couples should fully understand what rights they are creating and what rights they may be giving up when they enter into a CPT.

Homesteads

A homesteaded Florida residence can be included in a CPT in certain situations, but it also introduces some of the trust’s most complicated legal issues. Specifically, a CPT may affect creditor protection and the legal rules governing how the home passes at death. Work with an estate planning attorney experience in setting up homesteads in CPTs.

Last-minute trusts

As with many estate planning strategies, creating and funding a trust shortly before one spouse's death can create additional risks and uncertainty. Better to do your planning well before a health crisis.

No guarantee on tax treatment

The tax rules governing community property are well established. Florida's Community Property Trust statute is relatively new, however, so there is little direct IRS guidance and case law specifically addressing them.

Most estate planning practitioners believe the tax treatment should work as intended, but families should understand that some federal tax questions remain. As the aforementioned articles’ author states, in the unlikely event that CPTs are not recognized, couples with CPTs should be no worse off (except for the cost and time spend creating them).

Businesses and LLCs

Business interests, LLC membership interests, and closely held companies can sometimes be excellent assets for a Community Property Trust, since they often have substantial unrealized appreciation. But entity agreements, buy-sell arrangements, and valuation issues need to be carefully reviewed before transferring ownership interests into a trust.

Costs/benefits

Legal fees will vary widely depending on CPT’s complexity. As a rough guideline, you can expect several thousand dollars in legal fees and very possibly more if business entities, homestead property, or more extensive estate planning work is involved.

For families with several hundred thousand dollars or more in unrealized gains, even a partial reduction in future capital gains taxes could justify the legal cost of exploring a CPT.

Planning before drafting

A Community Property Trust should almost never begin with the estate planning attorney drafting documents, but with financial planning. A CFP® professional can help you address such critical questions such as:

Which assets have the largest unrealized gains?

Which assets should stay out of the trust?

Is a sale of assets after the first spouse's death likely?

Do you or your spouse have estate planning or family circumstances that make a CPT less attractive?

How does this strategy effect your charitable planning, retirement income planning, and legacy goals?

Are there enough potential tax savings to justify the added complexity and cost of a CPT?

CPTs are not an asset protection strategy and by no means are they a one-size-fits-all solution. They’re a specialized planning tool intended primarily to address capital gains taxes. Their potential complexity underscores how important it is to work with a well-coordinated team that includes a financial advisor, accountant, and attorney experienced in Florida CPTs.